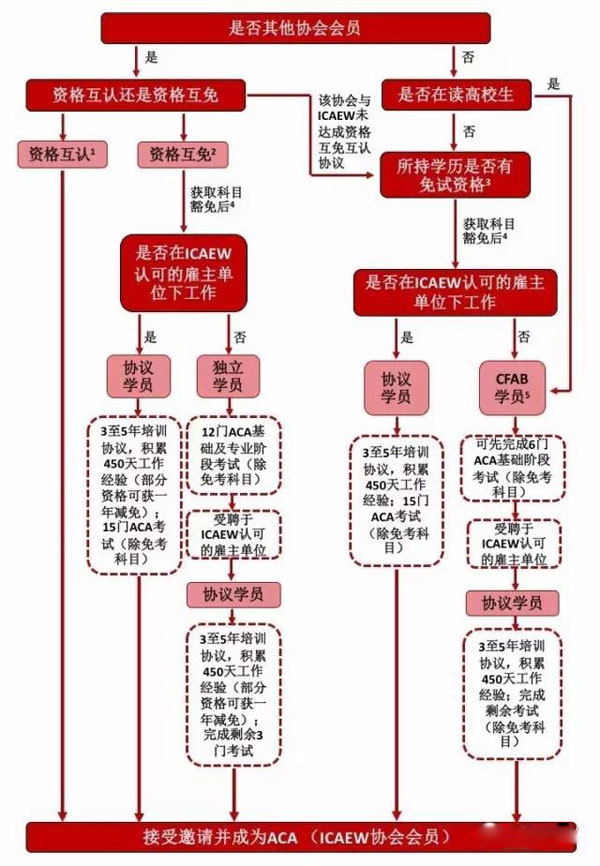

ACA:审计与鉴证备考|审计师与管理层的责任

·Why can assurance never be absolute? ·The expectations gap ·Nature of work undertaken ·Directors’responsibilities under the Companies Act 2006 ·Assurance providers’responsibilities 一、Why can assurance never be absolute? Testing and sampling The fact that testing is used–the auditors do not oversee the process of building the financial statements from start to finish.The fact that assurance providers would not test every item in the subject matter. Reliance on controls The fact that the accounting systems on which assurance providers may place a degree of reliance also have inherent limitations.The fact that the client’s staff members may collude in fraud that can then be deliberately hidden from the auditor or misrepresent matters to them for the same purpose. Nature of the financial statements The fact that most audit evidence is persuasive rather than conclusive.The fact that some items in the subject matter may be estimates and are therefore uncertain.It is impossible to conclude absolutely that judgemental estimates are correct. Quality of auditor judgements ·The fact that assurance provision can be subjective and professional judgements have to be made. 二、The expectations gap This is the difference between what users think the auditor does and what the auditor actually does.This is often because users are not aware of the nature of the limitations on assurance provision,or do not understand them and believe that the assurance provider is offering a service(such as a guarantee of correctness)which in fact he is not. Assurance providers need to close this gap as far as possible in order to maintain the value of the assurance provided for the user.This is done in a variety of ways,for example: issuing an engagement letter spelling out the work that will be carried out and the limitations of that work(which we shall look at in the next chapter)and by regularly reviewing the format and content of reports issued as a result of assurance work. 三、Nature of work undertaken 四、Directors’responsibilities under the Companies Act 2006 Safeguarding assets It is therefore for them to take reasonable steps for the prevention and detection of fraud andcompliance with laws and regulations.To carry out this responsibility they need to implement systems and controls to safeguard thecompany’s assets and ensure that the systems and controls operate effectively. Books and records of the company The directors are legally responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the company.This requires records of: ·The cash payments and receipts What the payments and receipts relate to The assets(including non-current assets and inventory)???? ·The liabilities Preparation and delivery of company financial statements The directors are required to prepare financial statements and must give a true and fair view of the affairs of the company at the end of the accounting period and of the profit or loss of the company for that period.In preparing those financial statements,the directors are required to: ·Select suitable accounting policies and then apply them consistently ·Make judgements and estimates that are reasonable and prudent ·Comply with applicable accounting standards ·Prepare the financial statements on the correct basis(Going concern) ·Once the financial statements have been prepared,it is the directors’responsibility to ensure:???? They are laid before the members of the company in general meeting and delivered to Companies House within the specified time. 五、Assurance providers’responsibilities General The responsibility of the external provider of assurance services is determined by the requirements of any legislation or regulation under which the engagement is conducted,????he terms of engagement for the assignment,which will specify the services to be provided????ethical standards and quality control standards Statutory audit Under the Companies Act 2006,it is the external auditor’sresponsibility to form an independent opinion on the truth and fairness of the annual accounts,confirm that the annual accounts have been properly prepared in accordance with the Companies Act 2006,state in their audit report whether in the opinion the information given in the directors’report is onsistent with the annual accounts. CA 2006 also grants auditors certain rights to enable them to fulfil their responsibilities.Examples of these rights are: ·The right of access at all times to the company's books and accounts ·The right to obtain any information necessary for the audit from any employee of the company ·The right to attend any general meeting of the company. Non-assurance services A firm is only responsible for providing the services specifically negotiated with management.Such engagements do not result in the firm taking responsibility for any aspects of the company’s operations or procedures.For example,a firm may be engaged to perform services additional to the audit such as: ·Assisting the company with the maintenance of its accounting records ·Assisting the company with preparing management information ·Preparing the financial statements of the company ·Preparing the corporation tax return of the company The key point is that management retains the overall responsibility for all of these matters;the firm is employed as a support to management,providing expert assistance. 来源:微信号【于濮铭】,由中国ACA考试网【www.aca.cn】整理发布,若需引用或转载,请注明来源! |